UK growth rate at two-year high

Last month’s release of first-quarter gross domestic product (GDP) statistics confirmed the UK economy has now exited the shallow recession entered during the latter half of last year, while survey evidence suggests private sector output has continued to expand across the past two months.

The latest GDP data published by the Office for National Statistics (ONS) showed the UK economy grew by 0.6% during the January to March period. This figure was above all forecasts submitted to a Reuters poll of economists with the consensus prediction pointing to a 0.4% first quarter expansion and represents the fastest quarterly rate of growth since the final three months of 2021.

ONS said that growth was driven by broad-based strength across the services sector with retail, public transport and haulage, and health all performing well; car manufacturers also enjoyed a particularly good quarter, although construction activity remained weak. In addition, the statistics agency noted that the first-quarter data was likely to have been boosted by Easter falling in March this year compared to April last year.

Data from the closely-watched S&P Global/CIPS UK Purchasing Managers’ Index (PMI) suggests the recovery has continued in the second quarter as well. While May’s monthly release did reveal that the preliminary composite headline Index fell to 52.8 from 54.1 in April, this latest reading was still above the 50 threshold that denotes growth in private sector activity.

Commenting on the findings, S&P Global Market Intelligence’s Chief Business Economist Chris Williamson said, “The flash PMI survey data for May signalled a further expansion of UK business activity, suggesting the economy continues to recover from the mild recession seen late last year. The survey data are consistent with GDP rising by around 0.3% in the second quarter, with an encouraging revival of manufacturing accompanied by sustained, but slower, service sector growth.”

Inflation data dampens rate cut hopes

Chances of the Bank of England (BoE) sanctioning a June interest rate cut have declined significantly following last month’s smaller-than-expected drop in the rate of inflation.

Following its latest meeting, which concluded on 8 May, the BoE’s Monetary Policy Committee (MPC) voted by a seven to two majority to leave Bank Rate unchanged at 5.25%. The two dissenting voices, however, both preferred a quarter-point reduction and comments made by policymakers after the meeting did appear to suggest a first rate cut since 2020 was edging ever closer.

Speaking just after announcing the MPC’s decision, BoE Governor Andrew Bailey made it clear that the Bank does need to see “more evidence” of slowing price rises before cutting rates. But he once again struck a relatively upbeat note on future reductions adding he was “optimistic” things were moving in the right direction.

Comments subsequently made by BoE Deputy Governor Ben Broadbent also seemed to be potentially paving the way for rates to be cut soon. Speaking at a central banking conference, Mr Broadbent suggested that, if things continued to evolve in line with the Bank’s forecasts, then it was “possible” rates could be cut “some time over the summer.”

Last month’s release of inflation data though appears to have dashed hopes of an imminent cut. Although the headline annual CPI rate did fall sharply – down from 3.2% in March to 2.3% in April, primarily due to a large drop in household energy tariffs – the decline was less than had been expected, with both the BoE and economists polled by Reuters predicting a drop to 2.1%.

The next two MPC announcements are scheduled for 20 June and 1 August. While an August rate cut does still appear to be a distinct possibility, most analysts now agree that a June reduction looks increasingly unlikely.

Markets

At the end of May, equities were in mixed territory as new inflation data from the eurozone and the US was digested by investors. Inflation stateside came in as expected, while eurozone data was higher than anticipated, fuelling speculation over the pace of rate cuts in both regions.

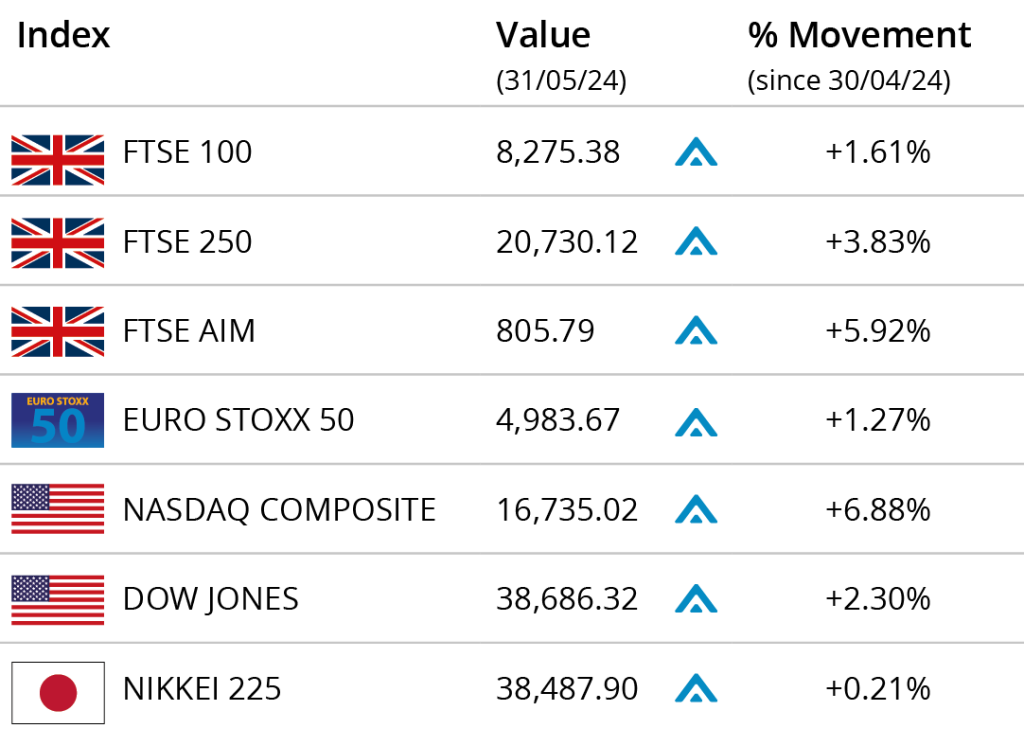

In the UK, the FTSE 100 index closed May on 8,275.38, a gain of 1.61% during the month, while the FTSE 250 closed the month 3.83% higher on 20,730.12. The FTSE AIM closed on 805.79, a gain of 5.92% in the month. The Euro Stoxx 50 closed the month on 4,983.67, up 1.27%. In Japan, the Nikkei 225 closed May on 38,487.90, a small monthly gain of 0.21%. At month end, the index traded higher as reports circulated of plans for major investments by government-backed pension funds and other large institutional investors.

Across the pond, at the end of May, newly released government data showed that during Q1 the US economy grew at a slower pace than initially estimated and higher than expected jobless claims also weighed on sentiment. The Dow closed May up 2.30% on 38,686.32, meanwhile the NASDAQ closed the month up 6.88% on 16,735.02.

On the foreign exchanges, the euro closed the month at €1.17 against sterling. The US dollar closed at $1.27 against sterling and at $1.08 against the euro.

Brent crude closed May, trading at $81.38 a barrel, a loss during the month of 5.69%. The price dipped in May primarily due to concerns over future demand. Gold closed the month trading around $2,348 a troy ounce, a monthly gain of 1.79%.

(Data compiled by TOMD)

Consumer sentiment continues to rise

Although official retail sales statistics for April did reveal a larger than expected decline in sales volumes, more recent survey data does point to an improving consumer outlook as households become more optimistic about their finances.

According to ONS data published last month, total retail sales volumes fell by 2.3% in April following a 0.2% decline in March. ONS said sales fell across most sectors as poor weather reduced footfall but added that it was confident its seasonally adjusted figures had accounted for the timing of the Easter holidays.

Recently released survey data, though, does point to growing optimism for future retail prospects. May’s CBI Distributive Trades Survey, for instance, reported a balance of +8 in its year-on-year sales volumes measure following April’s slump to -44. The CBI said May’s rise added to “the swathe of data pointing to an improvement in activity over the near-term” and suggested that falling inflation and continuing real wage growth will contribute to a “healthier consumer outlook.”

Data from the latest GfK consumer confidence index also revealed another rise in consumer sentiment. Indeed, May’s headline figure reached its highest level for nearly two-and-a-half years, as households took an increasingly positive view of their personal finances.

Wage growth remains resilient

Earnings statistics published last month showed that wage growth remains strong despite the recent slowing jobs market, although analysts do expect pay growth to moderate over the coming months.

The latest ONS figures show that average weekly earnings excluding bonuses rose at an annual rate of 6.0% in the first three months of 2024. This figure was the same as recorded in the previous three-month period, defying analysts’ expectations of a slight dip to 5.9%. After adjusting for CPI inflation, regular pay increased by 2.4% on the year, the largest rise in real earnings for over two years.

A survey released last month by the Recruitment and Employment Confederation suggests earnings growth remained high in April, with pay rates for temporary staff rising at their fastest rate in nearly a year. One factor driving this increase was April’s 9.8% minimum wage rise.

Research recently published by the Chartered Institute of Personnel and Development (CIPD) also found that employer expectations for private sector wage rises remain at the same level as reported three months ago. The CIPD did though say they expect employers to adjust their pay plans in the coming months as inflation falls and the labour market continues to slow.

All details are correct at the time of writing (3 June 2024). Written and supplied by The Outsourced Marketing Department.