UK growth stronger than expected

Figures released last month by the Office for National Statistics (ONS) showed the UK economy grew faster in May than had been predicted, while survey evidence points to a more recent post-election pick-up in business activity.

The latest gross domestic product (GDP) statistics revealed that economic output rose by 0.4% in May, twice the level that had been forecast in a Reuters poll of economists. May’s figure also represented a strong rebound from the zero-growth rate recorded in April, with a broad-based increase in output as the services, manufacturing and construction sectors all posted positive rates of growth.

ONS also noted that growth was relatively strong in the three months to May, with GDP rising by 0.9% in comparison to the previous three-month period. This represents the UK economy’s fastest rate of growth for more than two years.

Evidence from a closely watched economic survey also suggests private sector output picked up last month following a lull in the run-up to July’s General Election. The preliminary headline growth indicator from the latest S&P Global/CIPS UK Purchasing Managers’ Index (PMI) stood at 52.7 in July, slightly ahead of analysts’ expectations and up from a six-month low of 52.3 in June. Manufacturing output was particularly strong, with this sector expanding at its fastest rate in almost two and a half years.

Commenting on the findings, S&P Global Market Intelligence’s Chief Business Economist Chris Williamson said, “The flash PMI survey data for July signal an encouraging start to the second half of the year, with output, order books and employment all growing at faster rates amid rebounding business confidence. The first post-election business survey paints a welcoming picture for the new government, with companies operating across manufacturing and services having gained optimism about the future and reporting a renewed surge in demand.”

Fresh signs of cooling jobs market

Last month’s release of labour market statistics revealed further signs of a softening in the UK jobs market with pay growth easing and another drop in the overall number of vacancies.

Recently released ONS figures showed that average weekly earnings excluding bonuses rose at an annual rate of 5.7% in the three months to May. Although this was in line with analysts’ expectations, it did represent a modest decline from the 6.0% recorded during the previous three-month period and was the slowest reported rate of pay growth since the summer of 2022.

ONS said the latest release suggested pay growth is now showing ‘signs of slowing again’ although it also pointed out that, in real terms, wage growth still stands at a two-and-a-half-year high. Indeed, after adjusting for inflation using the Consumer Prices Index including owner occupiers’ housing costs, regular pay rose by 2.5% in the three months to May.

The data also revealed a further fall in the number of job vacancies, with 30,000 fewer reported in the April–June period compared to the previous three months. While at 889,000, the total is still significantly higher than pre-pandemic levels, this latest fall was the 24th successive monthly decline in the overall level of vacancies.

ONS highlighted other signs of ‘cooling’ in the labour market as well, with growth in the number of employees on the payroll said to be ‘weakening over the medium term.’ Additionally, while the latest release did show the unemployment rate unchanged at 4.4%, ONS noted that the rate has been ‘gradually increasing.’

The statistics agency also provided an update on its plans to improve reliability of the labour market data. A switch to a new version of its Labour Force Survey, which had been due to take place in September, has now been delayed until next year.

Markets

On the last day of July, US equities were supported as investors contemplated the latest move from the Federal Reserve to retain rates, with indicators from Fed Chair Jerome Powell that a September cut “could be on the table.”

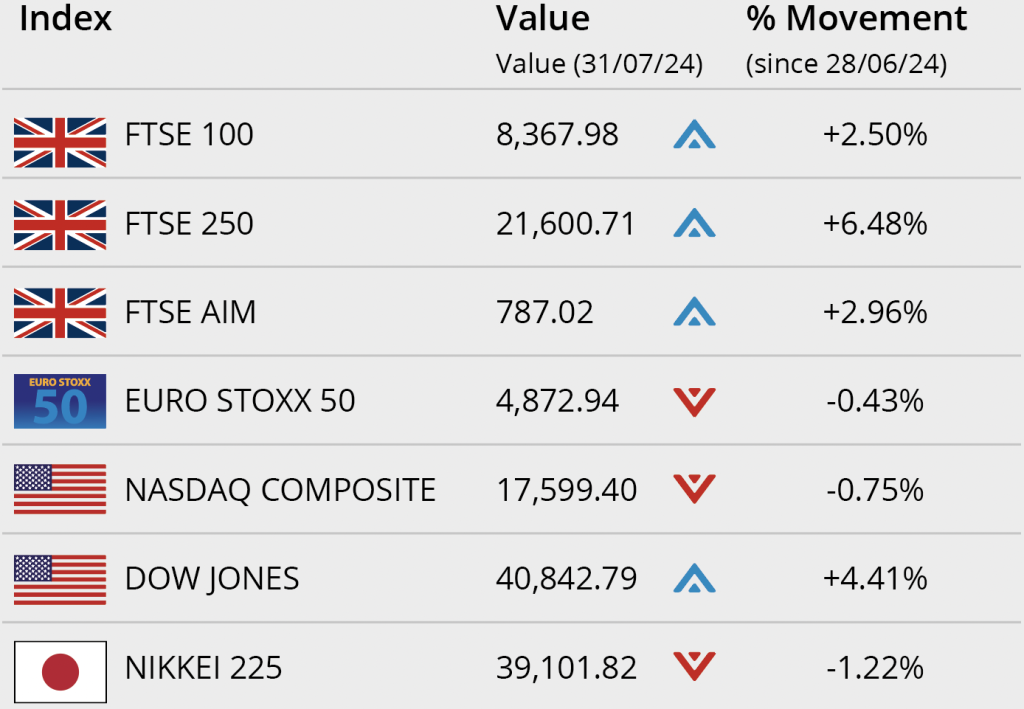

The tech-oriented NASDAQ responded positively after a challenging few days as initial earnings from some tech mega caps disappointed. The NASDAQ closed July down 0.75% on 17,599.40, while the Dow Jones closed the month up 4.41%

on 40,842.79.

The UK’s blue-chip FTSE 100 had a boost on 31 July, with a series of strong headline earnings supporting, while traders await the Bank of England’s next interest rate decision. The index closed the month on 8,367.98, a gain of 2.50% during July, while the FTSE 250 closed the month 6.48% higher on 21,600.71. The FTSE AIM closed on 787.02, a gain of 2.96% in the month. The Euro Stoxx 50 closed July on 4,872.94, down 0.43%. The Japanese Nikkei 225 closed the month on 39,101.82, a monthly loss of 1.22%.

On the foreign exchanges, the euro closed the month at €1.18 against sterling. The US dollar closed at $1.28 against sterling and at $1.08 against the euro.

Brent crude closed July trading at $80.91 a barrel, a loss over the month of 4.56%. With Middle East conflicts escalating, crude prices were impacted as markets closely watch geopolitical developments. Gold closed the month trading at $2,426.30 a troy ounce, a monthly gain of 4.09%.

(Data compiled by TOMD)

Headline inflation rate holds steady

Consumer price statistics published last month by ONS showed that the UK headline rate of inflation was unchanged in June defying analysts’ expectations of a slight fall.

According to the latest inflation figures, the Consumer Prices Index (CPI) 12-month rate – which compares prices in the current month with the same period a year earlier – remained at 2.0% in June. This was marginally above the 1.9% consensus forecast taken from a Reuters poll of economists.

The largest downward pressure on June’s CPI rate came from the clothing and footwear sector, which ONS said was due to a higher level of discounting in this year’s summer sales compared to 2023. Hotel prices, however, rose by a significantly greater extent this June than last year, while a comparatively smaller fall in the costs of second-hand cars also put upward pressure on the headline rate.

Just prior to release of June’s data, the International Monetary Fund (IMF) warned that the UK was among a number of countries witnessing some ‘persistence’ in inflation, particularly in relation to services inflation. The IMF added that this was ‘complicating monetary policy normalisation’ with the ‘upside risks to inflation’ raising the prospects of interest rates staying ‘higher for even longer.’

Cooler weather hits retail sector

The latest batch of official retail sales statistics revealed a decline in sales volumes after unseasonably cool weather deterred shoppers, while more recent survey data suggests the retail environment remains challenging.

Figures released last month by ONS showed that total retail sales volumes fell by 1.2% in June, following strong growth during May. ONS said June saw a decline across most sectors, particularly those sensitive to weather changes such as department stores and clothes shops, with retailers blaming poor weather and low footfall, as well as election uncertainty, for dampening sales.

Evidence from the latest CBI Distributive Trades Survey shows trading conditions have remained difficult, with its headline measure of sales volumes in the year to July dropping to -43% from -24% the previous month. The CBI described July as a ‘disappointing’ month for retailers, blaming a combination of ‘unfavourable weather conditions’ and ‘ongoing market uncertainty.’

The survey also found that the retail sector expects the weak outlook to continue this month, although August’s fall in sales volumes is forecast to be at a slower rate (-32%). The CBI also noted some glimmers of optimism, with a number of retailers expressing hopes for ‘an improvement in market conditions post-general election.’

All details are correct at the time of writing (1 August 2024). Written and supplied by The Outsourced Marketing Department.