Survey suggests recession already over

Official statistics released last month showed the UK economy fell into recession during the second half of last year, although more recent survey data does suggest the recession could already be over.

The latest gross domestic product (GDP) figures published by the Office for National Statistics (ONS) showed the economy shrank by a larger than expected 0.3% during the final quarter of last year. This follows a 0.1% contraction between July and September, thereby pushing the UK into a technical recession – defined as two consecutive quarterly falls in GDP.

ONS data also revealed the economy experienced little growth across the whole of last year. In total, it grew by just 0.1% over the course of 2023 which, excluding the pandemic years, represents the weakest annual rate of growth since 2009.

The start of this year, however, has seen clear signs of a rebound in growth prompting suggestions that the recession may prove short-lived. Bank of England (BoE) Governor Andrew Bailey, for instance, recently told MPs on the Treasury Committee that the economy is showing “distinct signs of an upturn” and that the recession looks like being the weakest of modern times “by a long way.”

Data from the latest S&P Global/CIPS UK Purchasing Managers’ Index (PMI) also paints a more positive picture reporting strong service sector growth and business optimism at a two-year high. The preliminary headline growth indicator also rose, up from 52.9 in January to 53.3 in February, beating analysts’ expectations and pointing to an upturn in economic growth.

S&P Global Market Intelligence’s Chief Business Economist Chris Williamson said, “The survey data points to the economy growing at a quarterly rate of 0.2-0.3% in the first quarter of 2024, allaying fears that last year’s downturn will have spilled over into 2024 and suggesting that the UK’s ‘recession’ is already over.”

High interest rates ‘under review’

Last month, the Bank of England (BoE) once again kept interest rates at a 16-year high, although policymakers did signal they were open to the possibility of lowering rates for the first time since the pandemic.

On 1 February, the BoE’s Monetary Policy Committee (MPC) announced it had voted to maintain Bank Rate at 5.25% following its latest deliberations. This decision, however, was not unanimous, with a three-way split emerging on the nine-member panel, two voting to raise rates by 0.25%, one preferring a similar-sized reduction and six opting to leave rates unchanged.

This meant the meeting was the first since 2020 when any policymaker had voted to reduce borrowing costs and the minutes also signalled a potential change of course – previous guidance stating that rates could rise again was withdrawn while a concluding sentence stated the MPC ‘will keep under review for how long Bank Rate should be maintained at its current level.’

Last month’s release of inflation data also raised hopes that the Bank may begin cutting rates soon. The headline annual CPI rate unexpectedly held firm at 4.0% in January, defying economists’ predictions that it would rise to 4.2%. Indeed, after release of the consumer prices data, investors put a 72% chance of a first interest rate reduction in June, with a 0.25% cut fully priced in for August.

While the past few weeks have seen several MPC members suggest there needs to be more evidence of weaker price pressures before rates can be cut, the BoE’s Governor did recently describe market expectations that the Bank would start reducing rates this year as “not unreasonable.” The latest poll conducted by Reuters suggests economists now expect the BoE to begin cutting rates in the third quarter, with a slim majority predicting the first cut will be delivered in August.

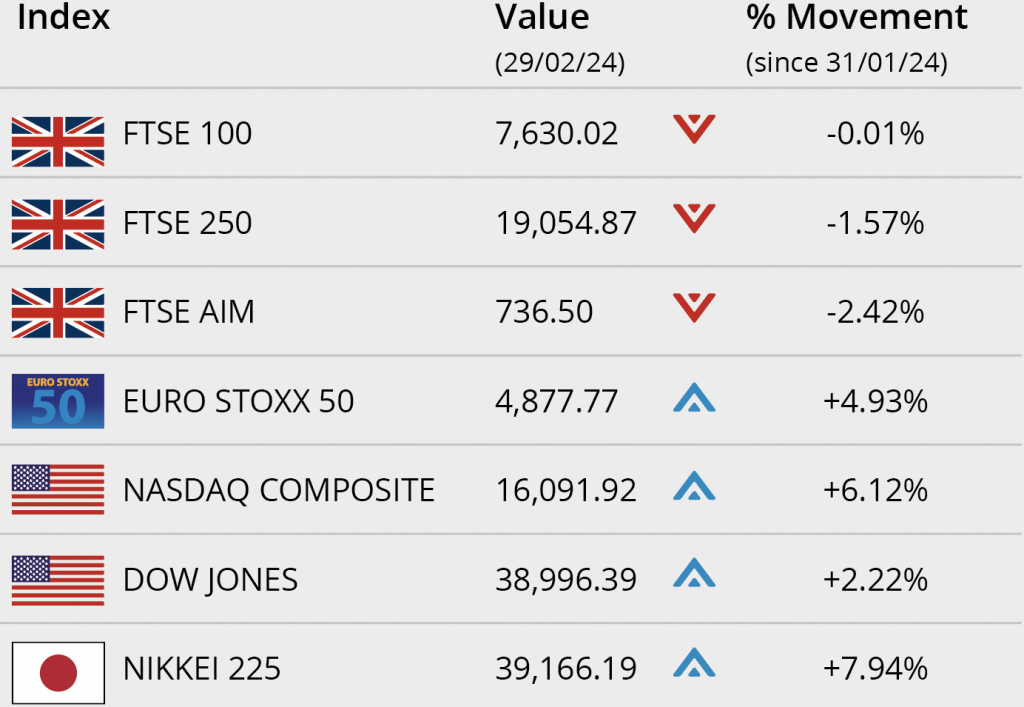

Markets

At the end of February, markets closed in mixed territory as investors processed a raft of data including US inflation, jobless claims and UK earnings.

Across the pond, data released at month end showed US prices increased at the slowest rate in nearly three years, keeping a June interest rate cut from the Federal Reserve on the table, while jobless claims rose. The Dow closed February up 2.22% on 38,996.39, with the tech-orientated NASDAQ closing the month up 6.12% on 16,091.92.

On home shores, the blue chip FTSE 100 index closed February on 7,630.02, a small loss of 0.01%, meanwhile the FTSE 250 ended the month 1.57% lower on 19,054.87. The FTSE AIM closed on 736.50, a loss of 2.42% in the month.

On the continent, the Euro Stoxx 50 ended February on 4,877.77, 4.93% higher. In Japan, the Nikkei 225 continued its bull run, concluding the month on 39,166.19, a gain of 7.94%. The index ended lower on the last trading day of the month ahead of the release of key US inflation data.

On the foreign exchanges, the euro closed the month at €1.16 against sterling. The US dollar closed at $1.26 against sterling and at $1.08 against the euro.

Brent crude ended the month trading at around $82 a barrel, a gain of 1.61%. The price per barrel has remained relatively stable within a narrow range over the last few weeks. Gold closed February trading around $2,048 a troy ounce, a small loss in the month of 0.25%. The price was supported by a softening in the US core price index at month end.

(Data compiled by TOMD)

Wage growth slows again

Earnings statistics published last month showed that nominal pay is now rising at the weakest pace for more than a year with survey data suggesting this decline looks set to continue.

According to the latest ONS figures, average weekly earnings excluding bonuses rose at an annual rate of 6.2% across the final three months of 2023. Although this figure was slightly ahead of analysts’ expectations, it was notably lower than the 6.7% figure recorded in the three months to November 2023 and represents the slowest rate of increase since the August to October 2022 period.

Survey evidence also points to an expected further slowdown in levels of pay growth. Data recently released by XpertHR, for instance, showed that the median basic pay settlement fell to 5.1% in the three months to the end of January; this represents a significant drop from the 6.0% rate recorded during the previous three-month period.

In addition, research from the Chartered Institute of Personnel and Development (CIPD) suggests employers expect to raise basic pay by an average of 4% over the coming year. This is well below the 5% figure reported across 2023 and signals the first drop in this measure for nearly four years.

Retail sales rebound in January

The latest batch of retail sales statistics suggest consumers have recovered some of their appetite for spending, with much stronger than expected growth in sales volumes recorded at the start of the new year.

According to ONS figures published last month, total retail sales volumes rose by 3.4% in January compared to the previous month. ONS said this growth, which was significantly above the 1.5% consensus forecast predicted in a Reuters poll of economists, was driven by strong supermarket sales and shoppers taking advantage of new year bargains.

Commenting on the day the figures were released, British Retail Consortium Director of Insight Kris Hamer called the news “promising.” He also suggested the growth reflected “rising levels of consumer confidence, as well as a boost from the January sales.”

The latest CBI Distributive Trades Survey also painted a more positive picture of the retail sector, with its headline measure of sales volumes in the year to February rising to -7% from -50% in January. This marked the slowest rate of decline in year-on-year sales for ten months. Looking further ahead, however, the survey did strike a note of caution with retailers expecting sales to contract at a slightly faster pace in March.

All details are correct at the time of writing (01 March 2024). Written and supplied by The Outsourced Marketing Department.